We stand in solidarity with the people of Ukraine! Learn More

Digital Transformation

November 20, 2023

6 Components For a Successful Digital Transformation in Banking

As the banking sector moves forward, it becomes a priority for banks to augment digital capabilities and leverage data analytics to deliver hyper-personalized services and superior customer experience. Customers continue to access financial and banking services across multiple channels, and when it comes to delivering an optimal customer experience, it is all about tailoring customer journeys to deliver custom and targeted experiences using data, analytics, artificial intelligence (AI), and automation.

Let’s dive deeper into the six components for a successful digital transformation in banking that can help you build a Future-Ready Bank.

1. Customer Centric Organization

The harsh reality is that a digital transformation in banking is either business-driven or product-focused – not customer-centric. However, customers nowadays are better informed and driven by the power of social networking websites; they require financial institutions to be customer-focused, provide better customer experience, and deliver value to customers in order to make them stay. This means that a starting point in order to build a future-ready bank is for them to base their decisions on a rich understanding of their customers’ needs and behaviors. By analyzing internal banking transaction data, surveying and interviewing customers and conducting external research, they will detect signals about which potential new products, features and applications customers would value.

Source: customersguide.cgap.org/

The move to a customer-centric business model is not simple, and the process is not swift. It requires emphasizing a portfolio of customers rather than a portfolio of products, with growth based on meeting customer needs and creating long-term customer value.

2. Modern Technology Landscape

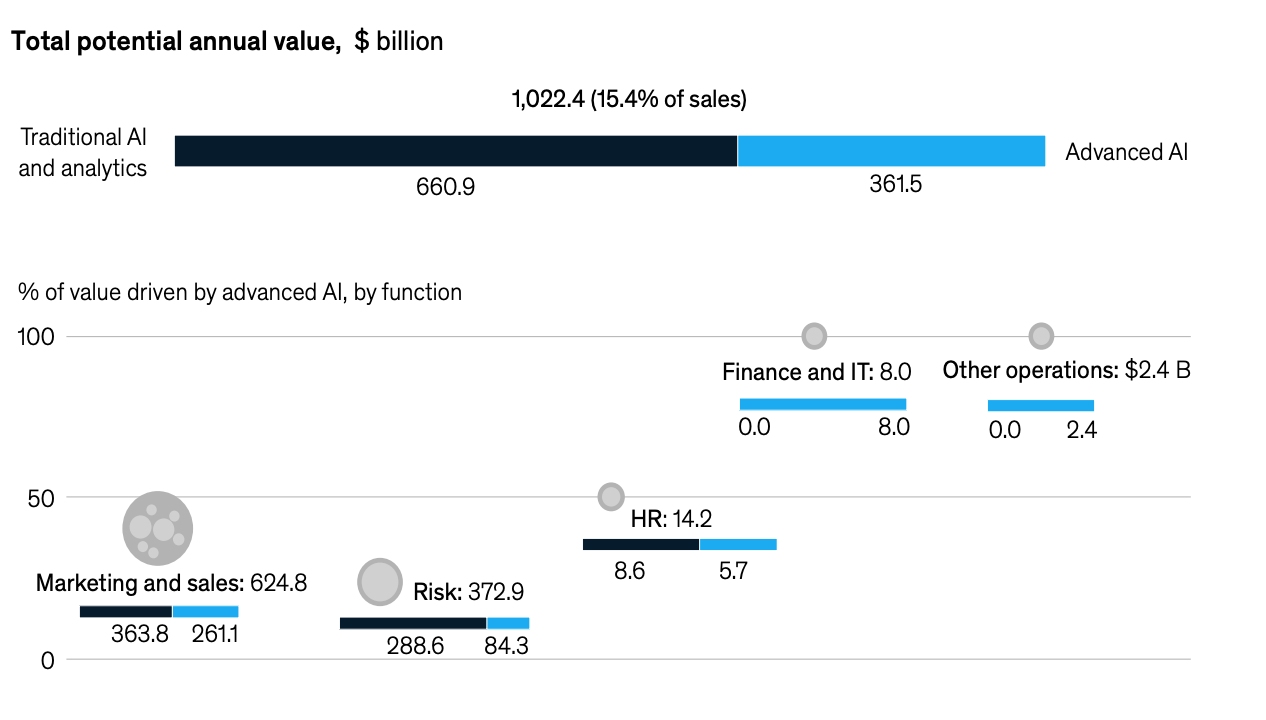

A modern, clean technology stack enables differentiated propositions andpowers improved cost efficiency. AI and chatbots are transforming the banking industry by providing customers with personalized banking experiences. Chatbots have become an essential part of customer service, providing assistance around the clock and resolving customer queries instantly. In contrast, generative AI is being used to provide personalized recommendations and insights to customers based on their transaction history. According to the PwC report, AI adoption in the banking industry is expected to rise from 16% to 77% by 2022.

McKinsey states that AI technologies can help boost revenues through increased personalization of services to customers and employees. It can help lower costs through efficiencies generated by higher automation, reduced errors rates, and better resource utilization, as well as uncover new and previously unrealized opportunities based on an improved ability to process and generate insights from vast troves of data.

More broadly, disruptive AI technologies can dramatically improve banks’ ability to achieve four key outcomes: higher profits, at-scale personalization, distinctive omnichannel experiences, and rapid innovation cycles.

Potential annual value of AI and analytics for global banking could reach as high as

$1 trillion:

Source: Building the AI bank of the future by McKinsey & Company

3. Agile & Adaptive Banking

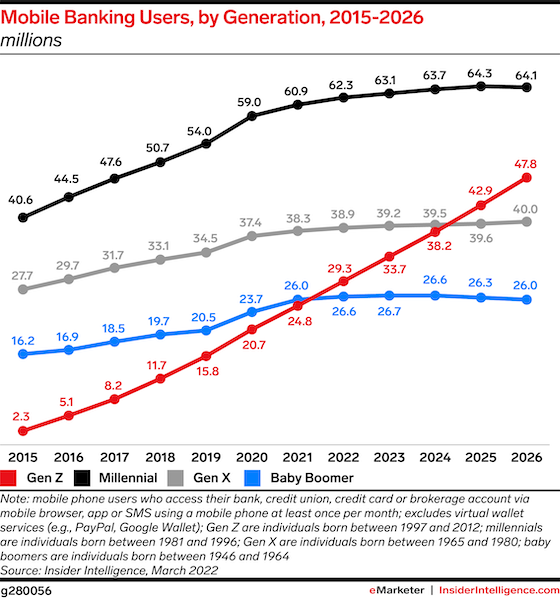

To be adaptive and agile, the banking industry must be competitive along with being able to offer new services to its customers with great speed and efficiency. According to the InsiderIntelligence report, at least 4 million Gen Zers will open banking accounts each year through 2026. In order to compete for the attention of those consumers, banks will need to meet them where they’re at: on social media and smartphones.

Source: InsiderIntelligence report

Mobile Banking

Following the urgent need for engaging with Gen Z’s individuals, Mobile banking has grown in popularity in order to provide an ability to conduct banking transactions on smartphones. Due to its superior convenience and ease of use, banks that are slow to adopt mobile banking risk losing their customers. Statista predicts that the number of mobile banking users will reach 1.75 billion by 2024.

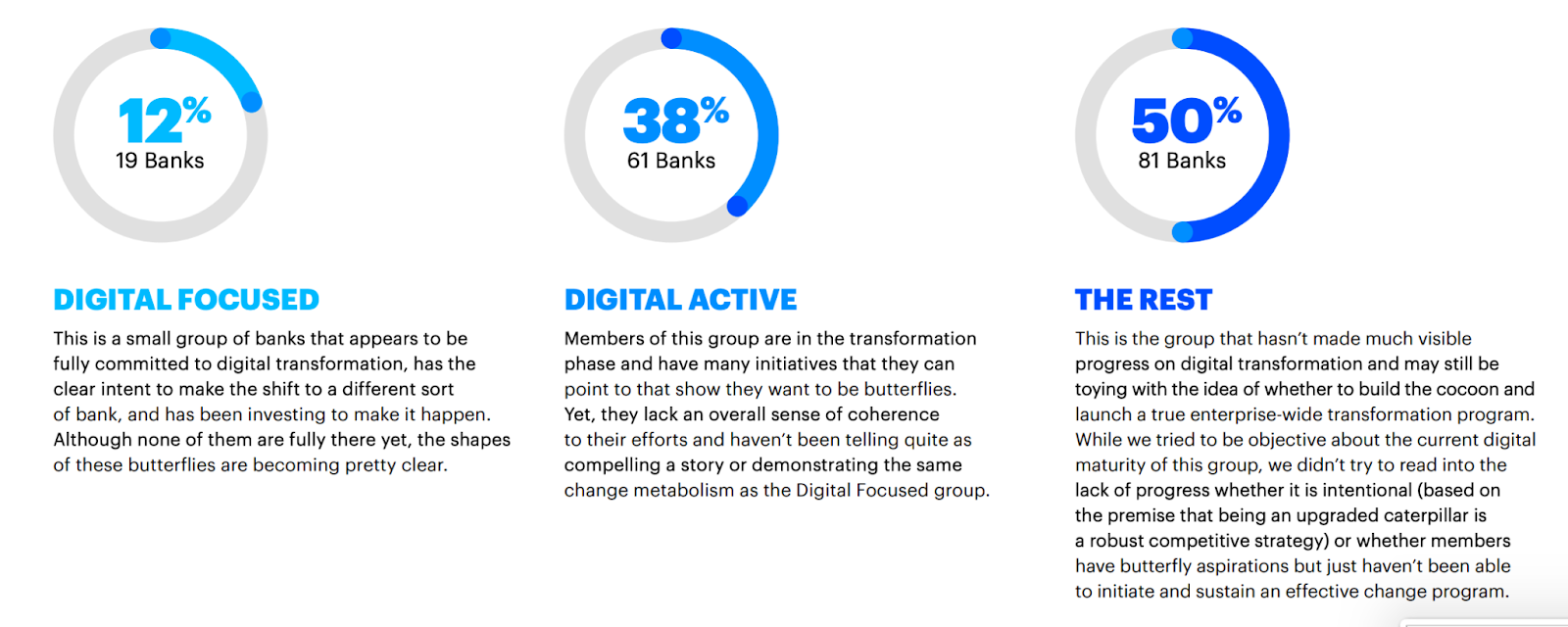

4. Digitally-focused Leadership

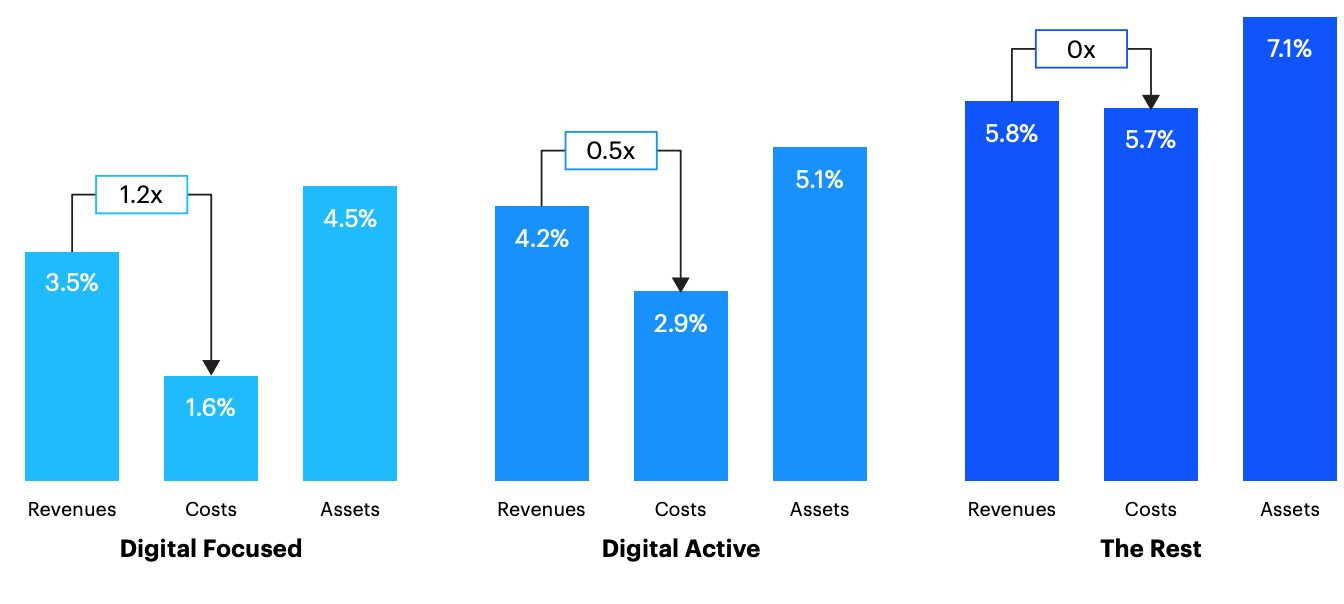

In one of their studies, Accenture discussed the importance of digital leadership in banking - in order to better understand the economic performance of banks and how it correlated with digital maturity. Accenture analyzed 161 retail and commercial banks from 20 countries, and ended up creating three segments:

Source: Does digital leadership in banking really matter?

As the next step, they attempted to determine whether digital leadership truly matters by systematically peeling the onion of economic performance and examining how those metrics correlate with the assessment of digital maturity. They found that the most highly valued and most profitable banks are in the Digital Focused group, but they are achieving their improved profitability through higher operating leverage that squeezes more profitability out of every dollar of assets. At the same time, The Rest created almost no operating leverage at all.

Source: Does digital leadership in banking really matter?

While the digital transformation in banking is hard, we have indeed moved into a period of volatility and industry change and digital maturity is at least one of the factors that will separate future winners from losers.

5. Cybersecurity

As digital banking grows in popularity, cybersecurity will become even more important. To protect customer data and prevent cyber attacks, banks will need to invest in advanced cybersecurity measures.

To identify and prevent fraud, advanced technologies, such as biometric authentication, artificial intelligence, and machine learning, will be used.

6. Clear Ecosystem Strategy

Digital transformation in banking is not just about technology. Organizations must first fundamentally rethink their business strategies. A thoughtfully crafted business strategy ensures that digital initiatives are aligned with overarching organizational goals, enabling banks to leverage technology for enhanced customer experiences, operational efficiency, and data-driven decision-making. Moreover, a strategic approach to digital banking helps institutions stay ahead of technological trends, mitigate cybersecurity risks, and adapt to regulatory requirements, fostering long-term sustainability in an increasingly digitized financial ecosystem.

The Science of a Digital Transformation in Banking

Once banks have a digital business strategy and an understanding of the experiences they want to deliver, CIOs and their teams can build the technology platforms to underpin their digital transformation. The monolithic legacy systems currently in place make it difficult for banks to respond to shifting customer expectations (by Deloitte).

In their article, Deloitte mentioned that the proof of a successful digital transformation in banking will be a future-ready bank built on a next-generation architecture that offers vastly greater capabilities for much lower cost. A core set of technical design principles will guide the development of this platform, including:

- Flexible and nimble architecture - in order to improve responsiveness to new business demands by designing components so new functions can be added to the IT landscape without affecting the customer or the organization.

- Efficient scalability to support high throughput - architecture should scale easily by component. Monoliths are becoming ancient history.

- Automated and digitized processes - simplifying then automating processes reduces turnaround and delivery times, reduces delivery costs, and improves customer service delivery and consistency across channels.

- Simpler and speedier development. IT leaders can employ Agile development to deliver capabilities incrementally by priority, reviewing and updating application architecture along the way to accommodate new capabilities. They can also leverage out-of-the box functionality and limit customization.

- Highly secure systems. Banks remain cybercriminals’ biggest target. IT leaders can limit their ability to hack and harvest data by segregating sensitive data and leveraging leading-class encryption technology.

- Customer-centric data. By building and leveraging a consistent version of customer data, IT leaders can enable their banks to deliver highly personalized service, real-time recommendations, and a holistic view of the financial value of a customer.This approach also improves data privacy transparency and compliance.

Digital technologies are driving innovation, change and digital transformation in banking – Mobile banking, AI and chatbots, Open banking are just a few of the digital banking trends reshaping the industry. Customers are increasingly demanding more innovative and convenient banking services, and banks that are slow to adopt these trends risk losing customers. Contact Tech-Azur today to learn more about how we can help you build a Future-Ready Bank by adopting the above mentioned 6 components in your firm.